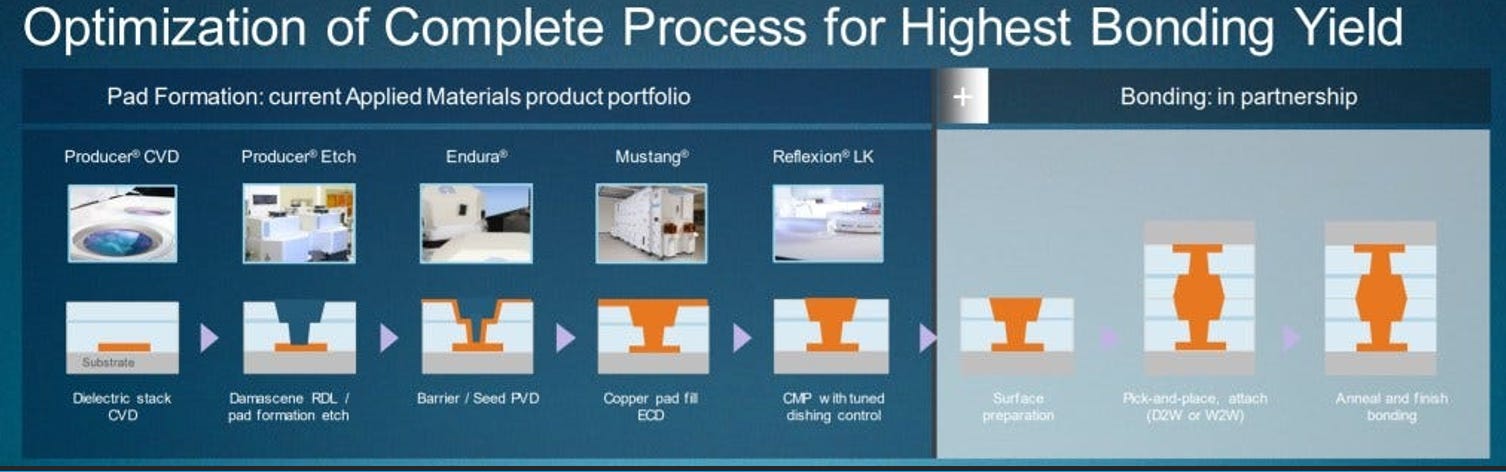

Advanced Packaging/Outsourced Assembly and Test (OSAT)

Packaging has significantly increased in importance for AI since it is a key enabler for increased I/O bandwidth. OSAT players stand to benefit as TSMC remains hesitant to expand packaging capacity

Investment summary

ASE Technology

19x 2026 PE

Leading OSAT globally with key operations in Taiwan

Strategic advantage of being located near TSMC leading edge fabs

Likely receiving majority (est >70%) of outsourced CoWoS work (i.e. WoS portion) from TSMC

Currently most CoWoS is fully packaged by TSMC end to end

However they likely outsource 10-15% of the WoS portion to OSAT like ASE

This outsourcing likely to increase as CoWoS demand increases

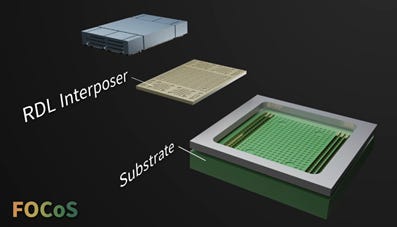

Also has own CoWoS-like technology with FOCoS (CoWoS-R like) and FOCoS bridge (CoWoS-L like)

Unconfirmed which customers are planning for adoption

Management noted multiple ASIC customers

With revenue contribution in 2026

Rumored to also be doing the packaging for NVDA Vera CPU and AMD Venice EPYC server

Also investing in testing to go along with packaging

Is higher gross margin (mid 30%s) than corporate average

Leading edge advanced packaging (including testing) contributes ~12% of ATM (assembly, test, materials) business or 8% of total revenue (2025)

Amkor

28x 2026 P/E

Key swing factor is Amkor’s $7b investment in Arizona, US

To go alongside TSMC fabs

Will be packaging Nvidia GPU as well as Apple M series initially

This likely is at the expense of ASE who currently is TSMC key partner in Taiwan

However, phase 1 (~$2b) is expected to be completed mid 2027, with production commencing early 2028

With phase 2 subject to customer demand

Currently single digit % of revenue attributable to AI

Rumored to be doing the packaging for Broadcom Tomahawk 6 switches and Nvidia GB10 for DGX Spark

TSMC

20x 2026 P/E

Gaining share in packaging driven by ‘Foundry 2.0’ company strategy

Synergies between foundry and packaging for higher yields

TSMC being conservative by offloading excess demand to OSAT players

Also outsourcing lower margin portions of CoWoS (i.e. oS)

However, may be too conservative, forcing ASIC customers to look elsewhere for advance packaging

Also as CoWoS-like packaging technology matures, should see increased competition from Intel IFS and other OSAT

Also shift to purely RDL interposer (no silicon interposer) should see share shift to OSAT

As well as shift to panel interposer in 2028+

King Yuan Electronics (KYEC)

26x 2026 P/E

Has most exposure to final packaged test for AI GPU

Likely does final package test for NVDA CoWoS sent from TSMC

ASE likely does the final package test for the CoWoS packages they do the WoS portion for (~10-15%)

Have increased capex to $37b (>100% of 2025 revenue)

Could see doubling of revenue in ~2 years

KYEC has the highest % revenue that is attributable to AI/HPC at 25% (2024)

Powertech Technology (PTI)

26x 2026 P/E

OSAT that specializes in memory packaging and test

Has strong relationship with Micron, SK Hynix and Kioxia/WD

Heavily investing in fan out panel level packaging for next phase of CoWoS innovation, i.e. CoPoS

Rubin Ultra (16 x HBM stacks + 4 reticle die stitching) would require much larger interposer than currently available

Scheduled to ramp late 2027/2028

Plans to increase capex to NT>$40b (US$13b) in 2026, up from NT$19b (US$0.6b) in 2025 for panel level packaging

A stock to keep in mind for 2026

Packaging overview

Semiconductor packaging refers to the final stage of semiconductor fabrication

Received finished dies on wafer from foundry

Packages chip into its final form ready to be soldered onto printed circuit board (PCB)

Commonly referred to as ‘back end’ process

‘Front end’ process refers to creating the transistor and metal layers on the wafer

‘Back end’ process includes everything done after that

There are multiple steps in the packaging process, e.g.

Dicing the chips from the wafer into singulated dies

Testing the chips for defects

Enclosing the chip in protective casing

Create electrical connections that the PCB can use (e.g. solder bumps)

Practical example

Customer produces dies on wafer at TSMC

The wafers go directly from TSMC foundry to ASE facility

The dies on wafer are tested using automatic test equipment (ATE) to identify ‘known good dies’ (KGD) (i.e. wafer sort test)

Then the dies are diced and singulated to individual dies using high precision saws/lasers

KGD are then packaged using the specified packaging method (e.g. flip chip, 2.5D, etc.)

Final packaged is then tested again using ATE (i.e. final package test)

May also include system level test and burn in test

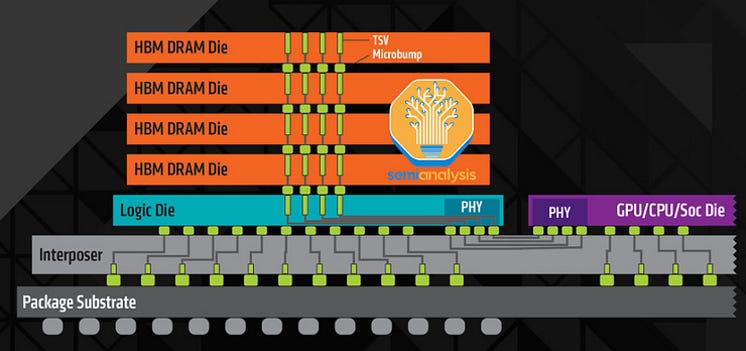

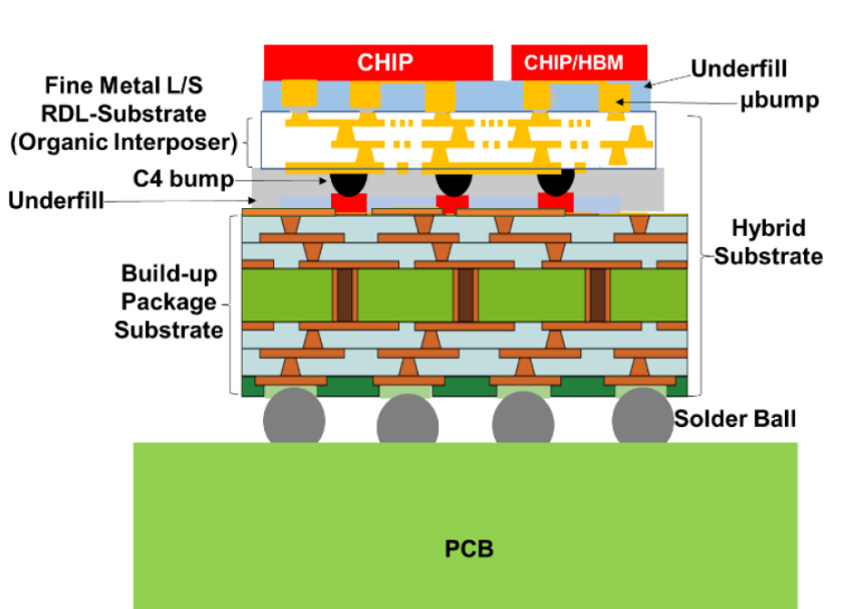

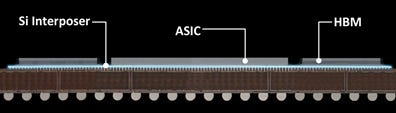

For heterogenous integration (combining multiple chips into a single package), it involves embedding the chips onto an interposer and/or substrate

Interposer is used to route interconnections between dies

Dies sit on top of the interposer

The interposer then sits on top of the substrate

Substrate is used to route electrical signals and power from the dies to the motherboard

The substrate then sits on top of the motherboard

Substrate connects to the motherboard via solder balls (i.e. ball grid arrays or BGA)

Outsourced semiconductor assembly and test (OSAT) refers vendors that do packaging and testing as a service

Historically, before the foundry/fabless model, packaging and testing was done inhouse by integrated device manufacturers (IDM) e.g. Intel, Samsung,

Types of packaging

Architecture

Contact Type

Wire

Contact Density

Substrate

Accuracy

Energy/Bit

5-101mm2

Organic/leadframe

20-10pm

1 OpJ/bit

Flip Chip

(1995)

Solder ball or copper

pillar

25-4001mm2

Organic/leadframe

10-5pm

O.5pJ/bit

TCB Bonding

(2012)

Heat compression force

Copper pillar

156-6251mlm2

Organic [Silicon

5-1 pm

0.1 pJ/bit

HD Fan Out

(2015)

1

Digita

RDL or copper pillar

500+1mm2

None

5-1 pm

O.5pJ/bit

Besi

Hybrid Bonding

(2018)

Hybrid bonding

Copper to copper

10K-1MM/mm2

None

0.5-0.1pm

<.05pJ/bit")

Wirebond

Chips are attached to a package substrate (or leadframe) and connected via fine wires (typically copper)

Relatively low cost and high volume

Generally used for >40nm process, for everyday electronics like TV, household appliances, etc.

Microcontrollers

Power devices

Analog integrated circuits

Many OSAT providers can do wirebonding

Compete on price, quality, track record, and low defective parts per million (DPPM)

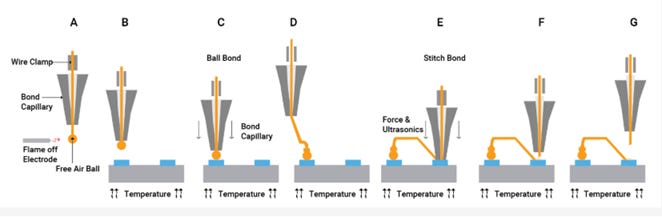

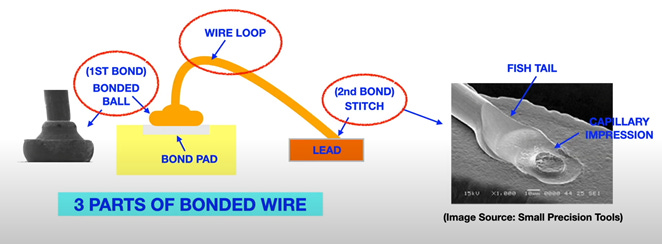

Wirebonding process

Process is done using a wirebonding machine

A bonding capillary (the pen like tool) has a tiny hole that feeds the wire through

The capillary pressures the wire onto the pad while applying force/heat/vibration

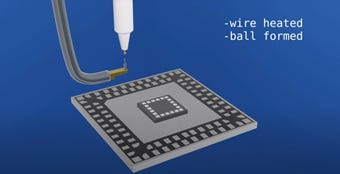

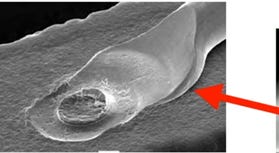

End of the wire from the capillary is heated to form a ball

Capillary then presses the ball onto the die’s bond pad, while applying force, heat and ultrasonic energy (i.e. thermosonic bonding)

Then wire is spooled out and carried over to the package leadframe forming a wire loop

Again applying thermosonic bonding to connect to the leadframe pad

The wire is pressed against the pad using heat, force and ultrasonic energy. Then clamped off forming a wedge/stitch bond

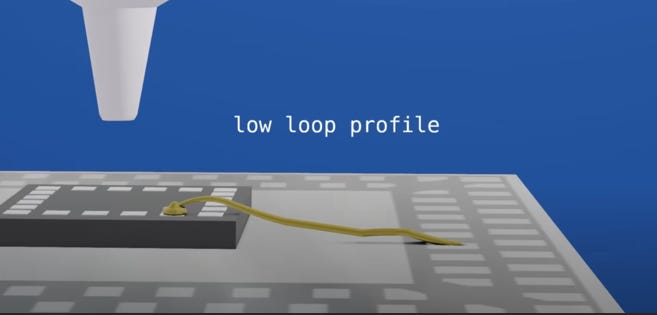

Low loop profile can be used for thinner package (<1mm)

This can be done by bending the wire forward and backwards using the capillary after the bond ha bee made on the die pad

However, there is limitation on how low the loop can be before damaging/breaking the wire

Alternatively, ‘reverse bonding’ can be done where the ball bond is first done on the substrate, and then on the die pad

Reduces stress on the ball neck

However, stitch bond cannot be directly done on the die pond bad

Because the capillary impact will damage the die surface

A bump must be first bonded on the die pad, and then the stich is bonded on top of the bump

Process is called ball (or bond) stich on ball or (BSOB) or stand off stitch bonding (SSB)

Dual in line package (DIP)

One of the earliest type of chip packages and is still widely used today

Use of leadframes which is a sheet of metal stamped to form leads

Have leads extending out from two opposite sites

The chip is attached to a die ‘paddle’ then wirebonded to the leads

Whole thing is then molded in plastic

Note the leads are designed to go through holes in the PCB and then soldered onto the other side (‘through hole’)

Typically 8-64 pins/leads with 2.54mm pitch

Small outline package (SOP)

SOP is a package with ‘gull wing’ leads extending from two opposite sides

Typically 8-48 pins/leads with ≤1.27mm pitch

Note the leads are L-shaped and soldered directly onto pads on the PCB

Quad flat no leads (QFN)

Unlike SOP, QFN has no leads

Instead connections are made via metal pads on the bottom of the package

Typically thinner profile than SOP

Because there are no leads, it minimizes space occupied on printed circuit board

Quad flat package (QFP)

Has leads extending from all four sides

Thus accommodating higher number of connections than SOP

Can be upwards of 300 pins/leads

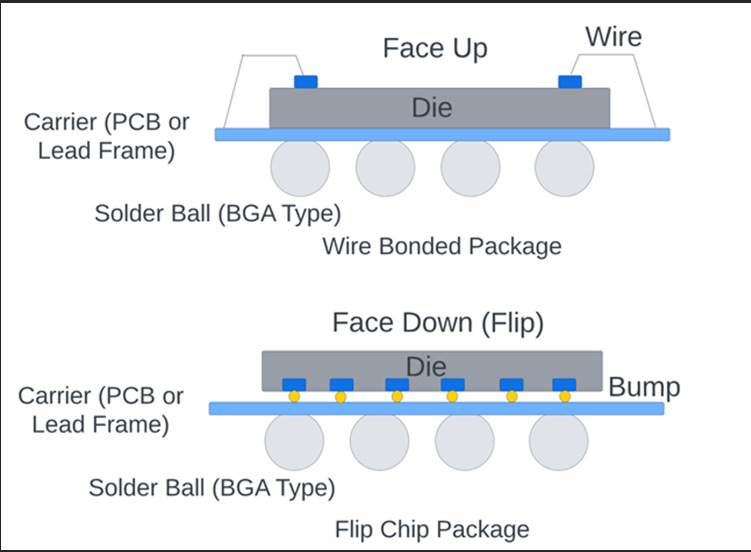

Flip chip

Introduced in late 1990s/early 2000s

Also known as Controlled Collapse Chip Connection or C4

Wirebonding is limited to the edge of the die

Whereas flip chip can use the entire surface area of the die

The chip is mounted directly onto a substrate (or even circuit board)

Uses solder bumps instead of wires (used in wirebonding) called ball grid array (BGA)

Connections are in the form of array of solder balls on the bottom of the package

Instead of wires coming out only on the edge

Advantages relative to wirebonding

Shorter signal path (0.1mm v.s. up to 5mm for wires) which reduces inductance and resistance

Important for high speed/high frequency applications (e.g. 5G, AI/HPC, etc.)

Higher I/O density

E.g. can have >100,000 solder bumps per die

Connections can be made across the entire area of the chip as opposed to just the sides for wirebonding

Eliminates bulking wire loops allowing for thinner, smaller packages

Direct contact with the substrate allows heat to dissipate more efficiently

Also allows the back of the chip (where heat is generated) to be exposed and cooled

Flip chip process

Solder balls (bumps) are placed across the entire surface of the chip while it is still on wafer

Wafer is then diced into individual chips

Then start with substrate (typically organic laminate)

Include various layers for redistributing signals and power

Chip bumps then aligned to substrate pads and bonded via solder reflow

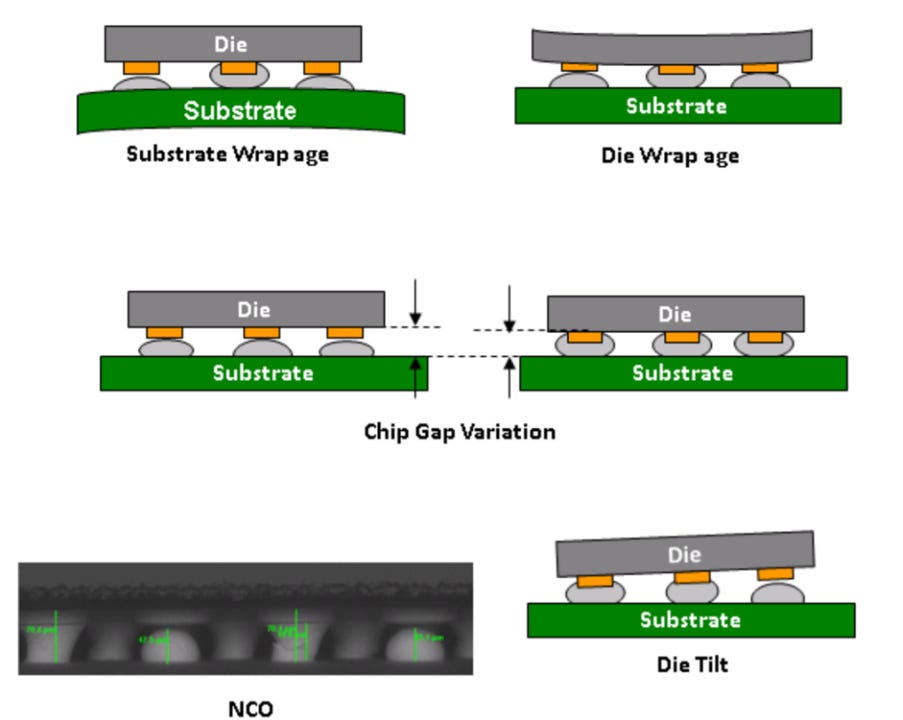

Some potential drawbacks of flip chip include

Warpage of either the substrate or die

Due to differing coefficient of thermal expansion (CTE) between different materials during reflow oven heating causing them to expand at different rates

Chip gaps caused by solder balls may making perfect contact with every copper pad

Die may not be perfectly flat

System in package (SiP)

System in package is a single package that contains 2 or more semiconductor dies

Rather than having separate chips on a large PCB

Effectively a ‘mini PCB’

May also include passive components such as resistors, capacitors, inductors, etc.

E.g. when transistors are turning on/off, there is a rapid change in current

Rapid change in current can cause a dip in voltage (like a momentary sag in pressure in a water pipe when you turn the tap on fast)

If the voltage drops too much, it can cause incorrect results (e.g. read ‘0’ instead of ‘1’)

A capacitor is a component that can store electrical charge

When the chip suddenly pulls current, the capacitor can quickly discharge that electrical charge (rather than pulling current from the power source)

This keeps the voltage stable

When things have calmed down, the capacitor recharges its electrical charge from the main power supply

This cycle happens millions of times per second, keeping the voltage clean and steady

In a SiP, the capacitor can be placed right next to the chip, sometimes even inside the package substrate or stacked on top

As opposed to on PCB where capacitors are further away

This provides faster response and more reliable performance

Other passive components used for

Prevent reflections and filter noise for RF and high speed signals

Reduce electromagnetic interference (EMI) using things like decoupling capacitors, ferrite beads or chokes, etc.

Tuning RF antenna

Supporting analog functions

Placing passives inside the SiP can save PCB footprint

Benefits

Save space by allowing shorter interconnections and higher density I/O

Also can integrate some components that would typically sit on PCB, e.g. DRAM, NAND, RF transceiver, etc.

Improved power/performance by shortening interconnections

Allow use of KGD instead of creating monolithic SoC

Common applications include

Connectivity module which includes transceiver for Bluetooth, WiFi, filtering, etc

RF front end modules which includes power amplifiers, switches, transceivers, filters, etc.

A variation of SiP is antenna in package (AiP)

Integration of antenna arrays on or in the package

E.g. for mmWave 5G modules

Manufacturing process

Wafer sort, grind and dice into singulated dies

Wafers are often thinned before dicing to maintain low package profile

Substrate (organic, ceramic or glass) is used which contains copper routing layers connected by TSV

Copper routing layers are used for signal and power delivery

Individual dies and passive components are placed onto the substrate

C4 bumps are created on the die

Dies are then aligned and bonded to the substrate pads

Then reflow and underfill

Epoxy mold then injected over the components and cured to form a hard plastic shell

Solder balls (BGA) are then attached to the bottom of the completed package

This allows it to be soldered onto the main circuit board

Substrate is then singulated into individual packages

SiP is often built in large panels for cost and scale efficiency

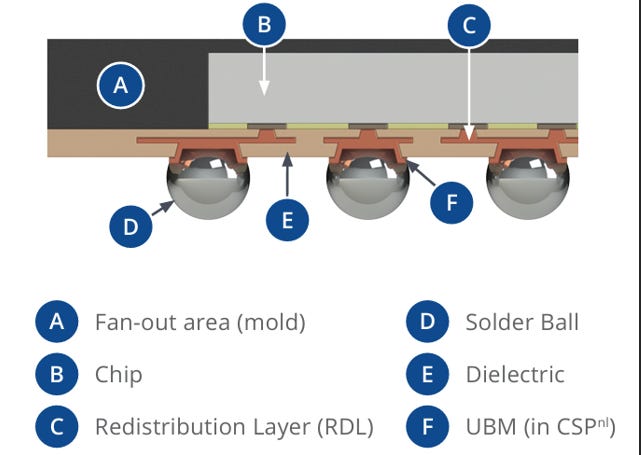

Fan out wafer level packaging

Fan out WLCSP allows the interconnections to be ‘fanned out’ beyond the surface of the die

Interconnections are made in a redistribution layer (RDL)

Solder balls are then placed on the top RDL layer, which connects to the PCB

Note there is no substrate layer

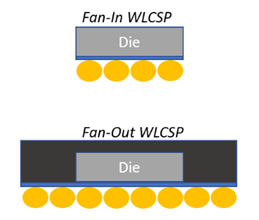

Wafer level chip scale packaging (WLCSP) means packaging the die while still on the wafer

Fan in WLCSP refers to a bumped die (i.e. effectively flip chip)

The package is the same size as the die

However the packaging is done while the die is still on wafer

RDL and solder balls are added directly on the wafer

As opposed to after the dies are singulated with flip chip

For fan in, the I/O is limited by the surface area of the chip

For fan out, the I/O can be expanded beyond the size of the die

Limited instead by silicon or organic interposer size

Can be very thin profile with high density interconnections

Commonly used for smartphone and wearables

Manufacturing process

Singulated dies are placed onto a temporary carrier (glass or silicon)

Epoxy mold compound is applied and cured which encapsulates the dies

Then grind/polish to expose the die pads

Redistribution layers (RDL) are then formed layer by layer

Dielectric is first deposited

Lithography used to print lines and vias

Copper is then deposited into the lines and vias to form connection to the previous layer (or die pads)

Finally, solder balls are placed at the top layer

Which forms connection to the printed circuit board later

Individual packages are then singulated using saw/laser

Alternatively, the RDL layers can be fabricated first (i.e. chip last)

Then dies are placed onto the RDL

bonding

Wafer molding

/ support wafer removal

RDL

Die

Chip-first method

Dice mounted on

metal-carrier

Wafer molding

/ carrier removal

RDL formation

Die

Resin

wafer

RDL

Singulation

Resin

wafer

External terminal formation

Singulation")

Panel level fan out (or panel level packaging or PLP) refers to the same process but just done on large rectangular panels

Fan out WLCSP is done on round wafers (300mm diameter)

But panels are much larger and rectangular (e.g. 600mm x 600mm) which is more suitable for packaging

Potential cost advantage compared to round wafers

However, more difficult to manage warpage and lithography uniformity

Examples include

TSMC integrated fan out (InFO)

ASE FOCoS

Amkor SWIFT

2.5D packaging

Allows multiple dies to be packaged side by side on passive interposer

Interposer provides high density interconnect

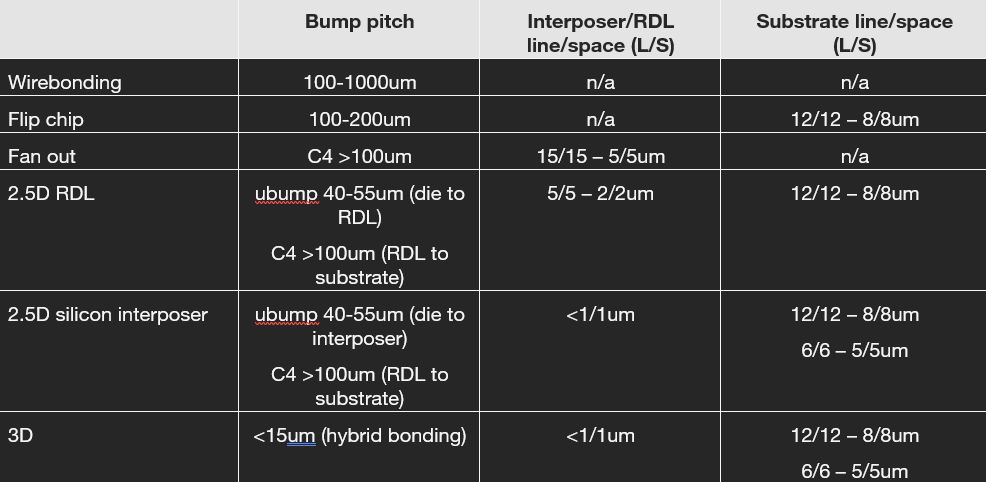

~1/1um L/S compared to 15/15 – 5/5um L/S for fan out

Effectively a more advanced version of fan out package

Larger interposers than fan out

Can package different types of dies together (rather than just chiplets)

Interposer can be either silicon or organic

Can include integrated passive devices (IPD) such as capacitors, inductors, resistors, etc., embedded directly into the interposer

Helpful for AI/HPC devices that drive very high current and fast frequencies

Embedded decoupling capacitors help flatten impedance and mitigate voltage droop

For silicon interposer, it is typically fabricated on silicon wafer using 130nm or 65nm lithography to making traces and TSV

For organic interposer, RDL layers are fabricated on morganic material

Less costly as avoids silicon

Avoids deep TSV etch + copper electroplating process for silicon interposer

Organic interposer have much shallower vias

Silicon interposer made at foundry line with foundry pricing/margins

However, has larger L/S of 5/5 – 2/2um v.s. 1/1um for silicon interposer

Suitable for devices that have moderate bandwidth needs

Can also support larger formats

Beyond 3x reticle size which is the current limit for silicon interposer

However still needs to fit equipment which is made for 300mm wafer

In the future, there is shift towards panel level packaging which uses large 300mm x 300mm or 600mm x 600mm square panels

Can also have silicon bridge embedded in RDL interposer (i.e. local silicon interconnect or LSI)

Silicon bridge used for interconnections between die to die

I.e. provides ultra dense connections where needed

With rest of the routing handled by RDL

Currently used for Nvidia Blackwell GPUs

Although require to manage warpage issues due to different coefficient of thermal expansion (CTE) between organic interposer and silicon bridge

Can use low CTE substrate resin

Or add dummy copper to balance stress

Interposer is then connected onto substrate

This part is either done by the foundry (i.e. TSMC) or can also be outsourced to OSAT

Manufacturing process

Start with silicon wafer

TSV lithography patterned and etched

TSV used to connect the dies and the package substrate

TSV then filled with copper

Then RDL traces and vias are patterned and copper plated

Dielectric (SiO2) deposited using PECVD

Traces and vias patterned using lithography and etched

Then copper plated

Repeated for each RDL layer

Photoresist applied and patterned to form copper pillar patterns

Copper pillars then plated and capped with solder

KGD logic and HBM dies now attached to interposer using flip chip and reflow

Flux applied on interposer

Flip chip bonders then place the die onto the interposer pad

There is room for misalignment for bump-based bonding as solder has capillary forces which allow for self-alignment

Baked in reflow oven

Flux residue is removed

Gap between die and interpose then filled with epoxy resin

Wafer baked again to cure the underfill

Top dies then encapsulated with resin for mechanical support

CMP is used to smooth the surface

Package is now flipped and thinned by grinding and polishing

Until TSV on backside of interposer is revealed

Backside of interposer plated and bumped with C4 solder bumps

Package then diced into singulated package

Interposer now attached to package substrate using flip chip process

Entire package then encapsulated with protective layer

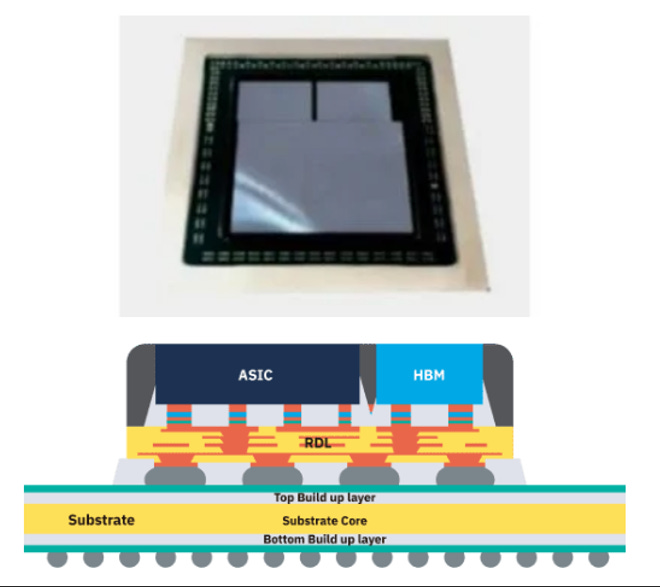

Substrate

Substrate provided by substrate providers

E.g. Unimicron, Ibiden, Nan Ya PCB, Kinsus, Ibiden, Shinko, AT&S, SEMCO, etc.

Substrate filled with copper wiring for routing

CoWoS typically uses Ajinomoto build up film (ABF) based organic substrate

ABF substrate typically made up of layer stack configured in X-Y-X where

X is the number of build up layers on the top and bottom

Build-up layers made from Ajinomoto Build-up Film (ABF) or similar material for fine line routing

Y is the number of core layers (often copper)

Provides mechanical support and power distribution

E.g. 5-2-5 substrate is made up of 5 buildup layers on top, 2 core layers, 5 bottom buildup layers

High end CPU packages may use 9-2-9 or 10-2-10 e.g. AMD EPYC, Intel Xeon, etc.

Can use less ‘build up’ layers if more of the routing is offloaded to the silicon interposer layer

Substrates are becoming larger with each CoWoS generation (i.e. CoWoS-S, CoWoS-R, CoWoS-R, etc.)

In the future, may start using glass substrates

Provides better stability at larger sizes

Also glass has better CTE matching with silicon

Expected timeline 2027

There is also developing of CoWoP (chip on wafer on PCB) which eliminates the need for substrates

This would be entirely done by OSAT houses

3D packaging

Taking an active die and packaging it on top of another active die

Typically will use hybrid bonding/TSV

Rather than C4 bumps or microbumps

3D packaging being used in

Sony CMOS image sensors

3D NAND stacking memory cell array and periphery circuit (e.g. YMTC Xtacking)

Backside power delivery networks

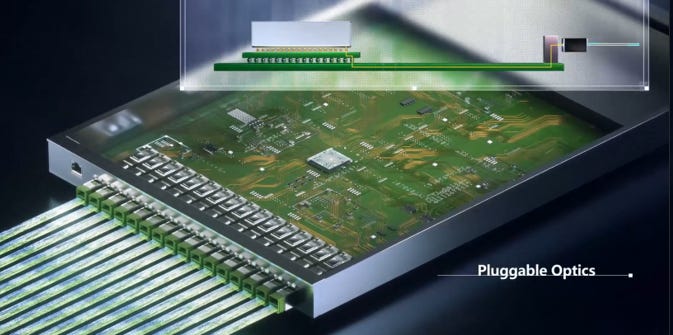

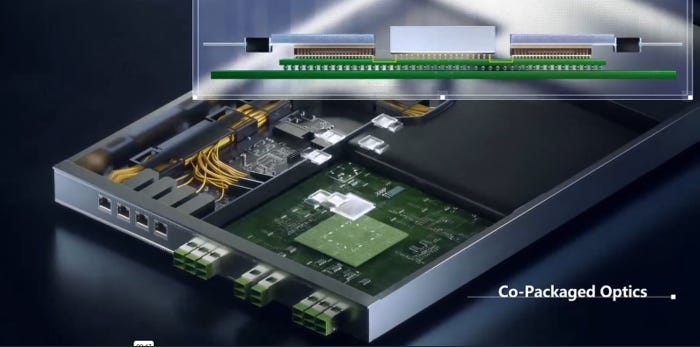

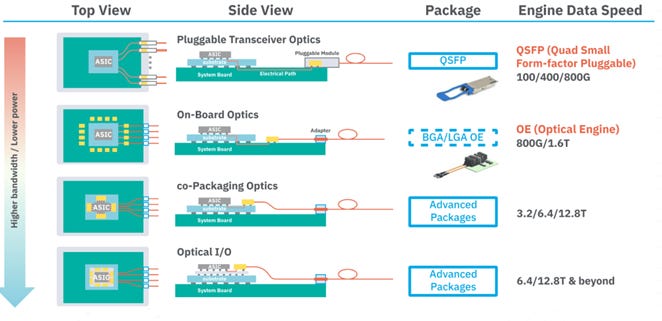

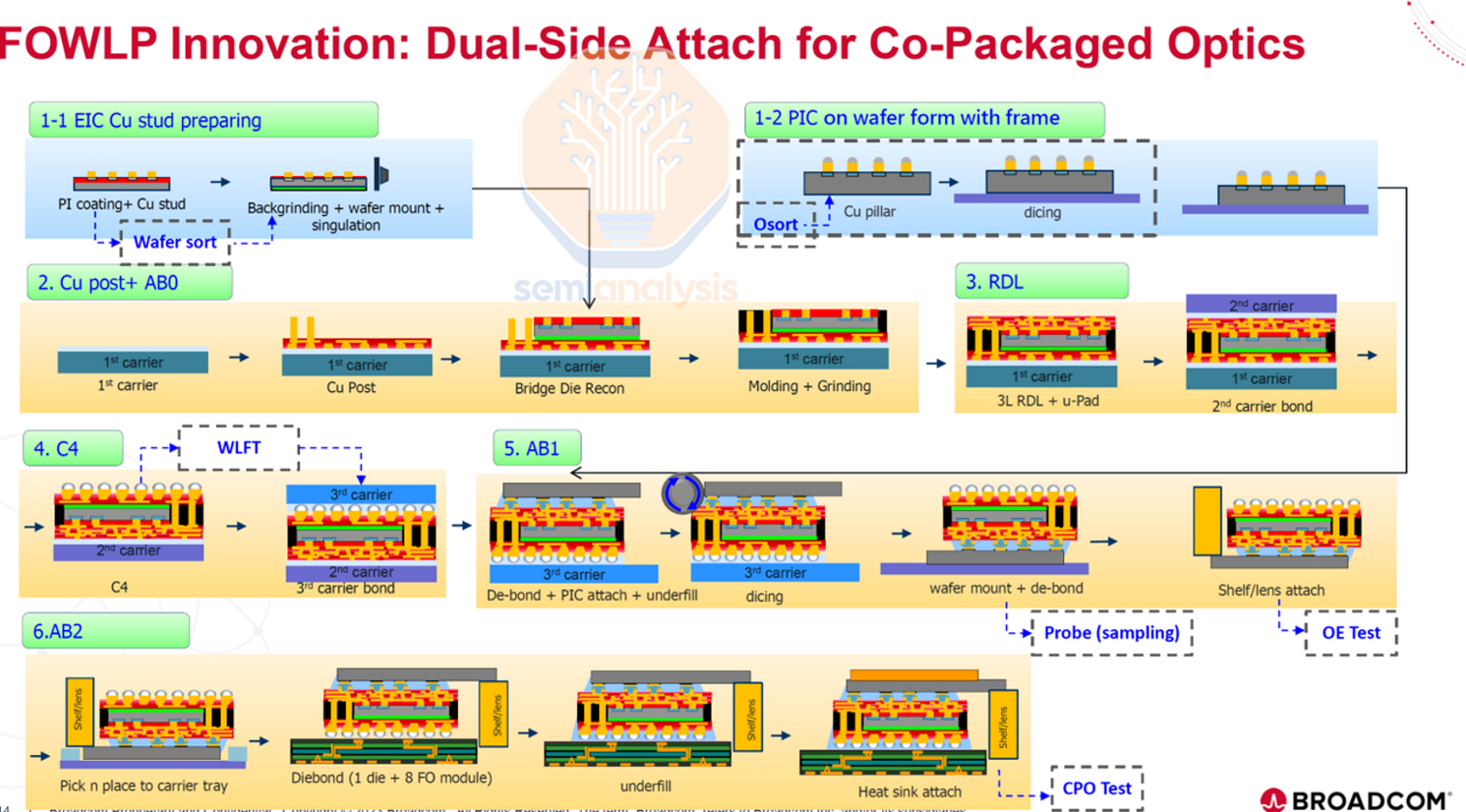

Copackaged optics

Silicon photonics offers data transmission with higher bandwidth and greater energy efficiency

Compared to conventional electronic integrated circuits which experience significant signal integrity challenges at high speed

Silicon photonics includes options from pluggables to integrated either on silicon interposer or substrate

Copackaged optics and optical I/O offer potential shortened electrical path to deliver even higher bandwidth

Mount photonics IC side by side with electrical die

Better efficiency (pJ/bit) and cost ($/Gbps) over pluggable optics

Copackaged optics est <5pJ/bit v.s. 20 pJ/bit for onboard optics and 30 pJ/bit for pluggable transceivers

One of the critical assembly steps in integrating the photonics IC is the optical fiber interface

Fiber arrays or optical connectors are aligned directly to the photonic chip coupling region

This could be edge‑coupling or vertical grating coupling, depending on design

Precision here is essential to minimize optical loss

Types of bonding

Wirebonding

Ultrasonic bonding

Uses combination of pressure and vibration between the bond wire and the bond pad

Produces cold weld between bond wire and pad

Used for aluminum wire to aluminum (or gold) pads

Thermocompression bonding (TCB)

Performed using combination of pressure and heat to form connection

Prevalent with gold wires for wirebonding

Bonding tools create ball bond at die site and wedge bond at the package pad site

But requires very high temperature of ~300-400 °C which can damage IC materials

Therefore not used prevalently today

Thermosonic bonding

Uses pressure, heat and vibration to make connection

Used when lower bonding temperature required (~180-250 °C)

Most common type of wirebonding today

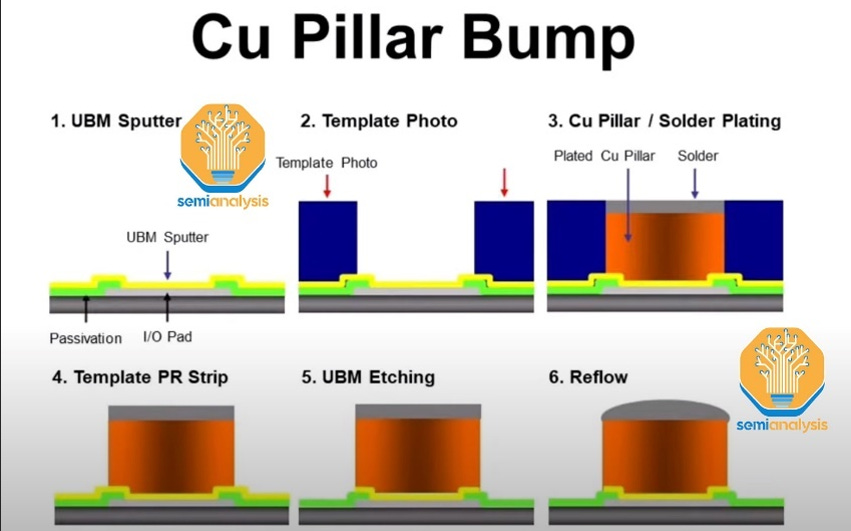

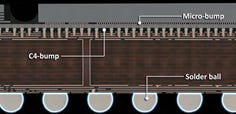

C4 bumps

Controlled collapse chip connection bumps (or C4 bumps) are relatively large solder bumps

Bump pitch 170-250 um

Bump height 70-100 um

Typically used to connect the chip to organic substrate using flip chip

Typically bonded via reflow soldering

A chemical agent (flux) is applied to the substrate copper pads to remove potential oxide layers present

Also reduces surface tension of the molten solder, ensuring it spreads evenly across the contact area

The stickiness of the flux also helps hold the chip in place before the reflow process

Die is then aligned so that the bumps match to the corresponding pads on the substrate

Done in batch process so many dies are placed all at once

Heat is applied to melt the solder bumps, forming a solid metallurgical and electrical bond (‘reflow’)

Done in reflow oven (or continuous reflow belt furnace)

Reflow refers to the process where the solder bumps are melted slightly and reform creating electrical connection

The remaining flux becomes resident that must be removed

Often flux is water soluble, so can be removed by water

Although some modern fluxes does not required to be cleaned afterwards

An insulating epoxy resin (underfill) is injected into the gap between the chip and substrate to provide mechanical strength

Microbumps

Fine pitch interconnects

40-130μm pitch

Max bump height of ~100um

Used typically between

Die to RDL

Die to interposer

HBM dies

Usually in the form of copper pillar bump structure

Better heat dissipation performance

Greater control of join diameter and stand off height compared with solder bump

Thermocompression bonding typically used here

Solder bumps are aligned to pads on the interposer/die/etc

Combination of pressure and heat (~200-300°C) is applied

Can also use rapid vibration which breaks up oxidation of metals on the copper bonding pads and solder balls

Thermocompression bonding used instead of solder reflow due to

Higher precision

Lower voiding

Better warpage control as avoids oven reflow process

Heat is applied from the top of the chip so only the chip and the microbump heats up

Minimizes substrate warpage

Compatible with temporary carrier wafers and fan out assembly flow

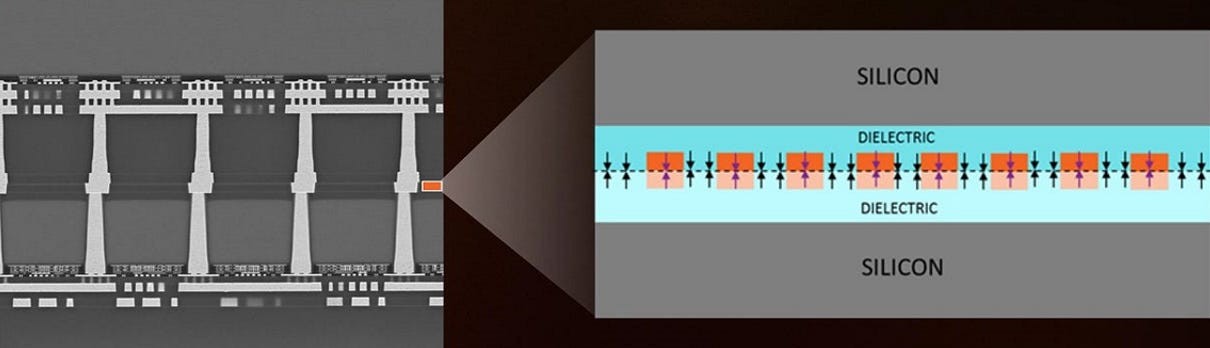

Hybrid bonding

Hybrid bonding allows to scale down to <10μm pitch

Approx 4-5x tighter pitch

Instead of solder, the interconnects are directly connected with copper pads (i.e. bumpless)

I.e. the top and bottom die are flush against each other

The copper pads are then connected to copper TSV which connects to the metal routing layers

Typically copper vias are patterned and electroplated within dielectric layer

Most commonly SiO2 or SiCN

Purpose of dielectric layer is to reduce interference between the vias

Can be completed either wafer to wafer (W2W) or die to wafer (D2W)

Wafer to wafer (W2W)

Two fabricated wafers are bonded directly together

Applications include CMOS image sensor, 3D NAND, BSPDN

Offers higher throughput

Only need to do alignment once per wafer v.s. once for every die on the wafer for D2W

However, not able to bin/test dies before the bond step

Thus typically used where the die yields are already high

A variation of W2W is ‘collective die on wafer’

The individual dies are KGD sorted and then temporarily bonded on reconstituted wafer

Then undergo W2W bonding

Copper vias and pads first formed

Wafer then aligned in chamber

Current W2W bonders can achieve alignment accuracy of <50nm

Then moved to heat chamber in vacuum where the wafers are pressed together with a small pressure for ~20 minutes to form the initial bond

Post bond inspection is done in situ via acoustics

If the alignment is insufficient, the bond can be reworked

Die to wafer (D2W)

KGD are singulated from wafer and individually attached onto another wafer

Die pick and placed by bonding tool

‘Pick up’ however introduces contaminants and particles

Also slower to pick and place at approx ~1500-2000 dies per hour (Besi)

Although throughput slower in practice to ensure high alignment accuracy

However, can test KGD so not wasting silicon

D2W bonder equipment providers include Besi, ASMPT, Shibaura Mechatronics

Wafer sort test done on wafer to identify KGD

Note that probing can cause small damage on the copper pad surfaces

Require to be smoothed out for hybrid bonding

Dies are then diced and singulated

Laser dicing is preferred to blade dicing due to less particles/contaminants

Plasma dicing can also work but it is much lower throughput

The bottom wafer then sits on a wafer chuck

The dies to be bonded sit on a tape frame

Robotic arm then picks up the individual die

Typically there are 2 x robotic arms working in parallel to increase throughput

Die is then aligned using optics (camera) and set of alignment marks

For 3um TSV pitch, alignment needs to be ±0.5um

The robotic arm then places the die in the desired location and applies a bit of pressure

One of the most time consuming steps is to physically place the die on the wafer

This is because extra time is required for high accuracy alignment

Also extra time is needed to ensure any trapped air between the bond surface is propagated out

Benefits

Direct copper connections have much lower resistance and therefore lower power when sending electrical signals

Drawbacks

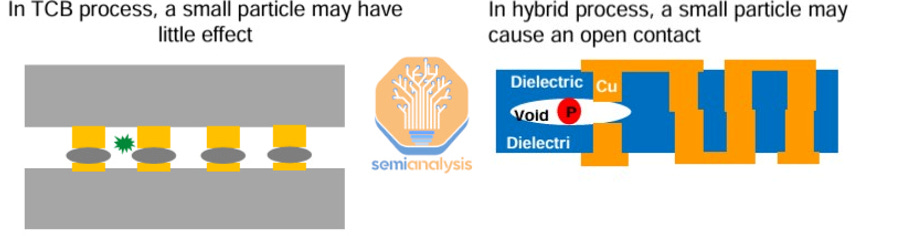

Very sensitive to particles which can lead to voids between the copper vias causing an open circuit

Require ISO 3 clean rooms

Common for foundries, but less common for OSAT players

Manufacturing process

TSV created in the silicon die through the transistor layer

Wafer coated with photoresist and patterned

TSV then etched using deep reactive ion etch (DRIE)

Barrier layer (e.g. titanium or tantalum) then deposited using CVD

Seed layer then deposited

Copper then filled using electrochemical deposition (ECD)

Chip is then flipped around and the backside of wafer is grinded until TSV is revealed

Copper pads are then formed using damascene process

Dielectric (SiO2 or SiCN) deposited

Holes for copper pads patterned over copper TSV and etched

Barrier and seed layer deposited, and then plated with copper

Chemical mechanical planarization (CMP) process used to grind down and smooth the dielectric surface

Bonding surfaces needs to be very smooth and planar

However, copper gets polished away fast than SiO2 dielectric by CMP

This means that the copper gets grinded down to a lower level than SiO2 i.e. over polishing (called ‘dishing’)

The exact profile of the dishing needs to be controlled

This can be mitigated by using a copper alloy instead of copper

Or use a proprietary CMP process with different slurries

The copper pads needs to either be recessed (>1um pitch) or protrude (<1um pitch) depending on the pitch of the copper pads

Typically recessed 5nm below the dielectric layer

This is to ensure that the copper does not get in the way of the dielectric to dielectric contact during annealing

Although if the copper is too recessed, then the copper to copper bond will not form

Two surfaces are now treated with plasma to ‘activate’ the surface

This enables the initial weak (Van Der Waals) dielectric to dielectric bond at 200°C in heat chamber

Then heat chamber is raised to 350-400°C for the copper to copper bond

The recessed copper expands at this temperature so that they contact

Thus the recession depth must be very accurate, as undergrowth will mean the proper bond is not formed

Testing overview

OSAT vendors purchase testing equipment such as

Automatic test equipment (ATE)

Wafer probe machines

Tokyo Electron is market leader

Ovens for burn in tests

Modules for system level test

OSAT vendors then charge a $ per hour for advanced devices, and $ per unit for high volume products

Testing typically commands higher gross margin due to lower capital intensity

Both KYEC and ASE testing have mid 30% gross margin

Compared to mid 20s% gross margin for packaging

Advanced packaging is higher gross margin

Testing gross margin is highly dependent on utilization

Average utilization is 65-70%

Testing can be categorized into phases such as wafer probe, final package test, etc.

Currently wafer probe is mostly done at Amkor and ASE

However, both are investing in final package test, including burn in and SLT

KYEC dominates in final package test

Industry themes

OSAT outsourcing gaining prominence

OSAT providers are taking larger share of the packaging and testing TAM due to

Fabless companies gaining share in their respective markets (e.g. AMD, NVDA, Apple, Qualcomm, etc.) over IDM

IDM increasing outsourcing (e.g. Intel, Samsung, Texas Instruments, etc.)

Fabless companies are purely design firms that outsource manufacturing to providers (e.g. foundry, OSAT, etc.)

Thus as fabless companies increase their share of sales in the market, the TAM for OSAT expands

IDMs are also increasing their outsourcing to OSAT

As devices get more complex, it requires increasing amount of R&D and capex resources to keep up with technological trends

OSAT have more scale to amortize fixed R&D spend over

OSAT can also maintain higher utilization on packaging equipment

Packaging equipment is quite fungible between packaging type and customers (Amkor, ASE)

Therefore, it is possible to better smooth out seasonality between different end markets (e.g. smartphone, PC, server/AI/HPC, auto, etc.)

And maintain high utilization of equipment

Cleanroom constraints

May need to ramp quickly for a new product

Inhousing packaging and testing would require expanding/building up new cleanroom space, ordering equipment (3-6 month lead time), etc.

OSAT provider can get packaging/testers up and running for a customer in weeks

IDM/foundries may have fabs in certain locations without the complementary packaging/test facility

Instead can outsource to OSAT in that region to avoid overseas shipment

IDM also tend to outsource low end packaging e.g. wirebond, etc.

Can reduce capital intensity by outsourcing packaging and test

To accommodate for increase capital intensity in front end manufacturing

Intel specifically may start increasing outsourcing since the operational split between design and foundry

IDM accounted for 35% of ASE revenue (3Q25)

For testing, outsourcing benefits include

Faster ramp

Potentially lower cost due to scale and higher utilization

Do not require to invest for peak demand

Although this would make OSAT revenue more cyclical to semiconductor swings

CoWoS

Customers will initially go to TSMC for turnkey service to guarantee yield and fast time to delivery

However as time goes on, more portions of packaging/testing can be outsourced as the technology matures

Regulatory control/tariffs

US Bureau of Industry and Security (BIS) created list of approved IC designers and approved OSAT companies

Certain high performance chips and ICs require BIS license to be exported/reexported/transferred outside US

However, there is an exemption if that chip is exported to OSAT company for packaging

List includes ASE Technology, Amkor, Powertech Technology, TSMC, UMC, Samsung, etc.

Generally does not include Chinese firms

Intention is to avoid sending advanced chips to China without a license

Where US export controls may be circumvented

E.g. if Nvidia Blackwell chips were to be packaged in China

ASE Technology has divested their China OSAT facility in response

US imposed sweeping tariffs to multiple countries globally on Apr 25

If OSAT packaged a chip and is shipped to US, tariffs may apply

Tariffs charged based on country of origin

This is generally where the imported product was ‘made’

I.e. where the last substantial transformation occurred

For chips, customs typically treat the packaged chip as originating in the country where the final assembly/packaging was done

Wafer made in Taiwan, packaged in Taiwan, sent to US

Will be classified as Taiwan origin. Standard duties will apply

Wafer made in Taiwan, packaged in China, sent to US

US customs likely treat as China origin

Because last substantial processing (packaging) was done in China

Semiconductors in China currently fall under Section 301 list, which is subject to 50% tariff

From 1 Jan 2025, the existing 25% duty on semiconductors from China doubled to 50%

Although tariff situation on Chinese semiconductors/electronics is in flux

Trump announced a new tariff to be imposed on Chinese semiconductors

But this additional tariff (in addition to the 50% existing tariff) is set to 0% initially, delaying any increase until Jun 2027

Wafer made in US, packaged in Taiwan, sent to US

Likely still treated as Taiwan origin, despite wafers made in US

Standard Taiwan duties will apply

Wafer made in US, packaged in Taiwan, sent to US

Likely still treated as China origin

Section 301 tariffs likely to apply

Wafers made in US, packaged in US

No import tariff apply at all

US CHIPS Act provides incentives for advanced packaging through direct funding grants

As part of the total $39b manufacturing incentive pool

Amkor has been awarded $407m in direct funding for their advanced packaging and test facility in Arizona (Dec 24)

Located close proximity to new TSMC wafer fab facility

Amkor has committed up to $7b total investment through multiple phases

Also eligible for the Advanced Manufacturing Investment Tax Credit scheme which is 35% for qualified investment in semiconductor manufacturing facilities including OSAT and advanced packaging

One Big Beautiful Bill Act increased tax credit from 25% to 35% (Jul 25)

Applies to depreciable tangible personal property related to manufacturing operations

Can be used to offset future tax obligations

US currently has ~3% of global advanced packaging capacity

Advanced packaging favors one stop shop vendors with both packaging and test facilities

Currently, individual GPU and HBM dies are individually tested. Then fully packaged together and tested again

This is the ‘final package’ test that is currently being outsourced to OSAT

However, there is talk of testing the package in various intermediate steps, e.g.

Testing silicon or RDL interposer (i.e. known good interposer)

Testing GPU on interposer

Then testing HBM on interposer

If testing is done in between packaging steps, then it makes more sense for both packaging and testing to be in one place

I.e. good for OSAT vendors that provide both packaging and testing (Amkor, ASE, PTI)

May be bad for pure play testing players like KYEC

Currently ~44% of KYEC revenue is in final package test (2024)

TSMC CoWoS

Currently majority of AI accelerators (+HBM) are packaged on TSMC CoWoS

TSMC monthly CoWoS capacity is estimated to be around 75-80k wspm (900-960k wafers annually)

It is rumored to increase to 120-130k wspm (1.4-1.6m) by end of 2026 ( https://www.trendforce.com/news/2025/12/08/news-tsmcs-cowos-l-s-reportedly-fully-booked-osat-partners-step-up-with-ases-cowop-in-focus/?utm_source=chatgpt.com)

“According to Commercial Times, TSMC’s AP8 facility in Southern Taiwan Science Park and AP7 in Chiayi have begun equipment move-in this quarter” (Dec 25)

NVDA currently dominates CoWoS capacity

ASE and Amkor are both certified OSAT providers

Scheduled for completion in mid 2027

Likely packaging technology used for each generation

Ampere (A100): CoWoS-S

Hopper (H100/H200): CoWoS-S

Blackwell (B200/B300): CoWoS-L

Rubin: CoWoS-L

Rubin Ultra: CoPoS (likely)

Rubin CPX: fan out (potentially)

Other CoWoS demand includes

AMD for MI series and Xlinix products

Broadcom for Google TPU, and also new Tomahawk switches (JPM)

ASICs from Meta, OpenAI, AWS

TSMC by default does the full flow CoWoS process including CoW and WoS portions

However, TSMC has outsourced some of the wafer on substrate (WoS) work to OSAT vendors

I.e. form C4 bumps on interposer to connect with substrate, reflow, underfill, encapsulate, then form solder balls on substrate for PCB mounting

ASE is believed to dominate the outsourced WoS work in Taiwan

Amkor is mainly targeting the US ramp in Arizona

This likely is to increase over time as demand continues to increase

TSMC rumored to have completely outsourced WoS portion for CoWoS-L (JPM)

TSMC is also outsourcing final package test to OSAT vendors such as ASE and KYEC

Currently TSMC likely does the wafer sort test (for known good GPU die), as they will need to do the CoW portion before sending to OSAT

ASE likely does final packaged test for the ~10-15% of CoWoS wafers which they do outsourced WoS for

KYEC likely does the other (majority) share for final packaged test

TSMC likely send the full CoWoS package to KYEC (rather than just CoW)

Rumored that TSMC will begin outsourcing the full CoWoS flow to OSAT beginning late 2026

TSMC motivated to outsource because

WoS portion is standard flip chip which has lower margin (below corporate average of high 50s%)

May start outsourcing CoWoS-S in preparation for more complex CoWoS-L

Also with panel level packaging set for mass production late 2027, there is risk of overcapacity for TSMC in wafer packaging

I.e. CoPoS (chip on panel on substrate)

However there are challenges with ‘through glass vias’ and mechanical stability

TAM

Total OSAT market is approx $40-50b annually

Includes both packaging and testing

Market is expected to grow low teens %

Driven by broader semiconductor market

Typically packaging/testing intensity as % of semiconductor capex remains relatively flat as single digit %

Although that may be increasing for advanced packaging and testing

Packaging typically is 75% of market v.s. testing at 25%

Packaging range from 15-25% gross margin, whereas testing can be 25-35% margin

Packaging tends to be more capital intensive, whereas testing is more IP intensive

Range is due to logic/IC (higher margin) v.s. memory (lower margin)

TAM is impacted by the share of outsourced v.s. inhouse

The outsourcing share continues to increase for the reasons aforementioned

Logic IDM limited to Intel and analog players

There is higher rate of inhousing from memory players e.g. Samsung, SK Hynix and Micron

Competitive landscape

ASE Technology is dominant player in Asia supply chains

Including Taiwan for advanced nodes

Amkor is leader in automotive. Also key OSAT provider to Apple

KYEC has been significantly ramping test capability for AI/HPC

TSMC, Intel and Samsung all have advanced packaging capabilities which they offer to external customers

Effectively reduces TAM of OSAT providers

However, all 3 partners with OSAT providers to expand capacity and outsources certain parts of it

OSAT providers help foundry/IDM ramp advanced packaging capacity faster

OSAT also have facilities globally that the foundry/IDM may not be present

Can outsource lower margin parts e.g. ‘wafer on substrate’

Packaging equipment is relatively fungible, so OSAT can achieve higher utilization on equipment

Allowing to provide advanced packaging cheaper

Whereas if TSMC overbuilds on CoWoS capacity, it less options available to change the capacity for something else

Also foundry/IDM may have more expertise in wafer + silicon interposer fabrication

But less expertise on organic interposer, substrate design, thermal considerations, assembly flow, testing, cost optimization, etc.

When choosing OSAT provider, the key considerations include

Scale

Whether the OSAT has enough scale to handle large volume devices

Capacity availability

Whether the OSAT can ramp up capacity when needed, e.g. AI/HPC

Packaging yield

Different OSAT providers will have different packaging yield

OSAT often provides a contractually ‘guaranteed’ yield

If yield falls below the guarantee, then the OSAT may provide damages

If yield is above the guarantee, then the OSAT may be provided a performance bonus

Packaging yield typically ranges between 90-95%

Packaging yield is becoming especially important for devices such as AI accelerators

The cost of scrapping a package is very high with GPU + 6-8 HBM stacks (each with 8+ DRAM dies)

Geographical location

Ideally the OSAT provider is located close to where the wafer is made

As the wafers need to be transferred from the foundry to OSAT provider

Customers prefer OSAT in close proximity to them

Customers often co design their devices with OSAT providers

Often pushing packaging technology to bleeding edge of what’s possible

Today, export regulatory controls and tariffs are also a consideration

Price

Typically priced on a per unit basis for packaging

For testing, it is based on cost per test hour basis

Pricing depends on

Design

Attachment rate

Long term loyalty

Trust

Technology

Overall solution

Sometimes customers may procure materials themselves, e.g. expensive substrate materials

Common to see price erosion clauses

e.g. 3-5% price reduction per year from expected efficiency gains

Some customers sign long term agreements to reserve capacity

Especially for capacity that requires new equipment investment

Substrate is provided by substrate providers

Ibiden (TSE 4062) provides substrate for NVDA

Other substrate providers include Shinko, Nanya PCB, Unimicron, and Kinsus

Substrate including insulating film supplied by Ajinomoto (TSE 2802)

China competition

There is increased competition for packaging in China

However, more so for mature nodes >7nm

However, China OSAT have begun investing for advanced packaging

Global OSAT vendors have also sold their China operations due to US BIS rules aforementioned

Non Chinese customers shifting OSAT needs outside of China (mostly to Taiwan)

Meanwhile, Chinese customers are sourcing locally

The net effect so far has been positive for non Chinese OSAT players

China is providing subsidies to build out its own packaging and test industry

Aligned with “Made in China 2025” initiative

Main China OSAT players include

JCET

Approx $5b revenue

Acquired STATS ChipPAC (2015) for flip chip capability

Include wirebond, flip chi, fan out, 2.5Dcapability

Tongfu Microelectronics

Approx $3b revenue

Has JV partnership with AMD in Suzhou and Penang plants

HT Tech (Huatian)

Approx $2b revenue

Affiliate with Hua Hong

Investing aggressively in high end packaging for AI

Also auto and memory

ASE Technology

Acquired Siliconware Precision Industries (SPIL) in 2018

Announced in 2016, but had to deal with regulatory hurdles

SPIL was #3 largest OSAT firm globally

ASE runs SPIL as independent company with its own customers and culture

Also acquired Universal Scientific Industrial (USI)

USI is a global Electronics Manufacturing Services (EMS) / Original Design Manufacturer (ODM)

Similar to Foxconn, Wistron, etc.

Does everything except for the final product assembly (e.g. assembling iPhone)

Does the final module assembly, taking the final packaged chip and producing a finished electronic module

E.g. takes the packaged chip and solders onto PCB

Also combines multiple PCB, modules, antennas, etc. into a self contained functional module

Has natural synergies with ASE/SPIL which does the chip packaging

Customers thus have one stop shop from wafer to final product (i.e. full turnkey service)

From packaging the chips

Testing the chips

Mounting the package on a PCB with other components

Testing the final product

Assembling the final product

Can reduce handoff and transit delays

Attractive for smaller IC design companies that want to minimize

Examples of electronic devices and module include

Smartphone, wearables and PC motherboards

Wireless connectivity modules (e.g. WiFi, bluetooth)

Display modules (e.g. flat panel display)

Power control modules

USI has been major backend SiP provider for Apple including

WiFi/bluetooth

Fingerprint sensor packages

Force touch controller modules

Apple Watch S Series SiP module

ASE Technology’s competitive advantages include

Scale

Largest OSAT provider in the world with ~1/3 market share

Able to provide customers with more assurance on capacity availability

Can handle large volume products (e.g. smartphones, wearables, IoT, auto, etc.)

Speed

ASE has historically demonstrated its ability to ramp up capacity to large volumes when needed

Is currently doing so now, with ~$3.5b equipment capex investment expected for 2025, almost double from $1.9b (2024)

Geography

Close to Taiwan supply chain

Taiwan is still where most of TSMC wafers are coming out from

Especially advanced ≤7nm nodes used for advanced packaging

ASE wants to continue expanding capacity in Taiwan

Following where the advanced wafers are being produced (i.e. TSMC foundry)

Believes that advanced packaging needs are rapidly evolving

Require R&D and operations to be in close proximity

Yields need to be constantly maintained generation by generation

Need to constantly tweak and change the configuration of packaging equipment

Believes it would be ineffective to do so from a satellite facility

Manufacturing

Have been investing in ‘lights out’ factories, i.e. fully automated lines

Can provide higher level of reliability and capacity

Approx 20% of capacity is fully automated (2023)

The entire factory process is also digitized

Capture data from every step of the process

Can share data with customers for transparency

Facilities and machinery capex has been increasing in intensity (as % of revenue)

Previously, facilities/machinery were generic and there was more commonality across factories

However, advanced packaging requires more specialized machine and equipment

Also with automation, the capex intensity is higher

Taiwan

Strategically located close to TSMC leading edge fabs

US

Currently no plans to build facility in US

Have been invited by customer to invest factory in US

Likely Apple and Nvidia

However, the economics is the main gating factor

Even with subsidies, the economics/return does not make sense

OSAT margins are quite slim, so less room to bear cost increases

However, SPIL (merged with ASE), was one of the announced partners to Nvidia $500b investment in manufacturing in US (Apr 25)

Mexico

Acquired some land in 2024

Will be able to service US

Malaysia, Korea, Singapore, Vietnam, Philippines

China

Disposed of China sites by the end of 2021

Due to regulatory export controls

Customers started to avoid packaging chips in China due to US BIS rules

4 plants located in Kunshan, Suzhou, Weihai, Shanghai

Primarily did traditional packaging

Sold to Wise Capital Road for US$1.46b

Go to market

Emphasize long term relationships with customers

Often co develop packaging innovation with customers (i.e. design for manufacturability)

Align packaging with customer roadmaps

Was first to launch 2.5D with AMD with Fiji GPU (launched 2015)

Had been working on 2.5D with AMD since 2007

E.g. if a fabless company is designing a new AI ASIC, ASE’s engineers might advise on bump layout or thermal solutions that align with ASE’s packaging capabilities

Will also co invest with customer

Customer may sometimes partially pay for new equipment

Or provide prepayment in exchange for reserve capacity

Promote engineering capability to industry via industry forums, e.g. SEMICON

Packaging

CEO has been very vocal about investment in silicon photonics packaging

Have been making investment in leading edge advanced packaging (LEAP)

Refers to ≤3nm node technology

Includes both advanced packaging (~80%) and testing (~20%) revenue

Includes FOCoS and FOCoS bridge revenue (3Q25)

~US$600m revenue in 2024, increasing to ~US$1.6b in 2025

Expected to increase >US $1b again in 2026

I’m estimating US$1.4b increase to $3.0b revenue in 2026

Contributing 11pcp of revenue growth and attributing 21% of packaging and test (‘ATM’) revenue

Note all the LEAP revenue is margin accretive

Test is ~35% gross margin (4Q24)

TSMS CoWoS outsourcing

Primarily does ‘wafer on substrate’ (WoS) portion of CoWoS

TSMC has stated that they don’t object ASE doing more of the CoWoS process

However gating factor is ramp up quality and reaching acceptable yield

ASE said it has TSMC support to guide them

Currently they are making investment for the CoW portion (2Q24)

Have engaged with multiple customers on FOCoS

Mostly from ASIC customers

Multiple customers have gained confidence on the technology over years of product development, trial and error, process materials, with different equipment, and reliability (2Q24)

Will start to see meaningful revenue come in 2026 (3Q25)

Will also be margin accretive

[Rumored AMD using ASE for Venice and other HPC products from late 2026 (JPM)]

[Also Nvidia Vera CPU]

Nvidia reportedly rumored to be working on packaging technology called CoWoP (chip on wafer on PCB) with SPIL

Eliminates the (expensive) substrate

Collaborate with Siemens Digital Industries Software OSAT Alliance Program to offer fully validated assembly design kit (ADK)

Adoption Siemens Xpedition Substrate Integrator and Calibre 3DSTACK technologies

Can significantly reduce FOCoS package planning and verification cycle times by about 30-50% in each design iteration

ASE offers the “VI Pack” which includes 6 advanced packaging solutions below

FoPOP

FOCoS

FOCoS bridge

FoSiP

2.5D/3D

Copackaged optics

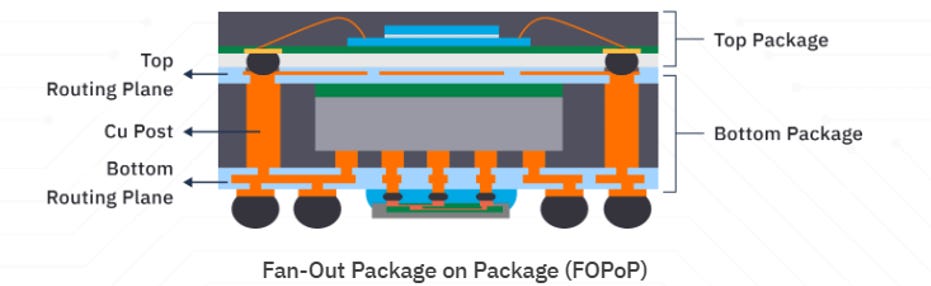

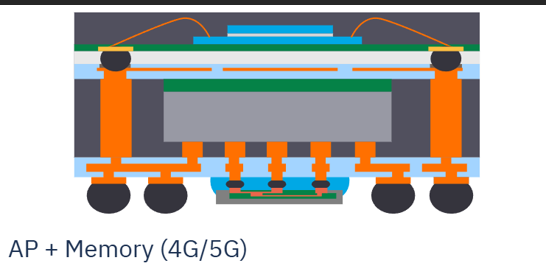

FOPoP (fan out package on package)

Combines fan out bottom package with a standard package mounted on the top

Benefits

Thinner profile and better electrical and thermal performance compared to conventional interposer based package on package

The bottom package eliminates the need for interposer

Almost 40% reduction in height over substrate based package on package

Higher interconnection density

Shorter interconnect length

The development cycle time and cost can also be reduced since top and bottom packages can be decoupled from each other

I.e. qualification, yield, sourcing, procurement timing and logistic handling

Allows for increased complexity due to RDL on both sides of the die

Used for

Mobile applications that require high density interconnections and thinner package form factor

Pluggable optical transceivers and copackaged optics because of higher bandwidth

Much shorter interconnection between the photonic integrated circuit and controller

Improves energy efficiencies from 25pJ/bit to 5pJ/bit

Note, a semi additive process is used to grow the copper post and RDL copper routing

Used instead of traditional subtractive process where you deposit a layer of material and etch away what you don’t want

Traditional damascene process is too costly for backend packaging

Start with temporary carrier (glass or silicon)

Then deposit ‘release layer’ (for debonding step later)

Deposit polymer dielectric like polyimide or benzocyclobutene (PBO) as RDL base layer

Thin copper seed layer is then deposited

Required for copper electroplating step later

Thick photoresist is applied. Lithography used to pattern traces in RDL layer

Copper electroplating used to deposit metal routing

Then remove photoresist and seed layer

Step repeated for desired number of RDL layers

Deposit seed layer and much thicker photoresist for copper vertical post

Pattern openings where post should be

Copper electroplating used to deposit copper post

Remove photoresist and seed layer

First die is then aligned and attached to RDL traces using flip chip process

Entire structure is then encapsulated with epoxy mold compound (EMC)

Backgrinding process used to remove the mold compound from the top to expose the vertical copper posts

Second RDL stack is now built on top of the structure

Temporary carrier (glass or silicon) is then removed from the structure by chemically dissolving or debonding from the ‘release layer’

Package is flipped, and grinded to reveal copper posts

Second die now attached

Then entire package is singulated and tested

FOCoS (fan out chip on substrate)

Have been in production since mid 2010s

Chips are integrated onto fan out RDL, which is then attached to substrate

Similar to TSMC CoWoS-R

No silicon interposer which reduces package cost

Less warpage compared to silicon

Due to differing coefficient of thermal expansion between silicon and organic substrate

Also ASE offers reinforcement rings to reduce warpage

Mechanical stiffeners (typically copper or stainless steel) that surround or partially encircle the outer edge of a large fan out package

Can pattern L/S (line/space) of 2/2um for RDL interconnect

I.e. line (copper trace) width of 2um and gap between adjacent traces of 2um

High I/O counts (>1,000)

RDL ~3um thick

FOCoS chip first used when integrating smaller number of chiplets

Fan out size typically under 1 reticle size with ~2-3 RDL layers

Shorter die to die interconnects due to avoiding microbumps

Dies are connect with direct copper vias through RDL

FOCoS chip last used when integrating multiple chips (e.g. ASIC + HBM stacks)

Support larger interposer (>1 reticle size) and potentially more RDL layers for very high I/O and bandwidth

FOCoS chip first

2 (or more) KGD chips attached onto carrier wafer

Entire structure is then encapsulated with epoxy mold compound (EMC)

Then mold grinded and planarized to expose chip

RDL layers then formed

Dielectric deposited onto mold surface

Seed layer deposited

Photoresist deposited and patterned for traces

Copper electroplating used to deposit copper

Remove photoresist and seed layer

Repeat for multiple RDL layers

Vias then patterned through dielectric and plated with copper to form connection

Form bumps on RDL layer that will connect to BGA subtrate

Package is then singulated and flip chipped onto BGA substrate

Underfill and overmold used to provide mechanical reliability

FOCoS chip last

Start with temporary carrier

RDL layers then built on the carrier

Microbumps (or copper pillars) are created on the die first

Microbump is ~125x smaller than C4 bump, and ~8000x smaller than solder ball

Then chip is mounted onto the RDL pads

Followed by thermocompression bonding

Mold compound is then used to create mechanical support

Solder bumps then mounted onto RDL to be attached to BGA substrate

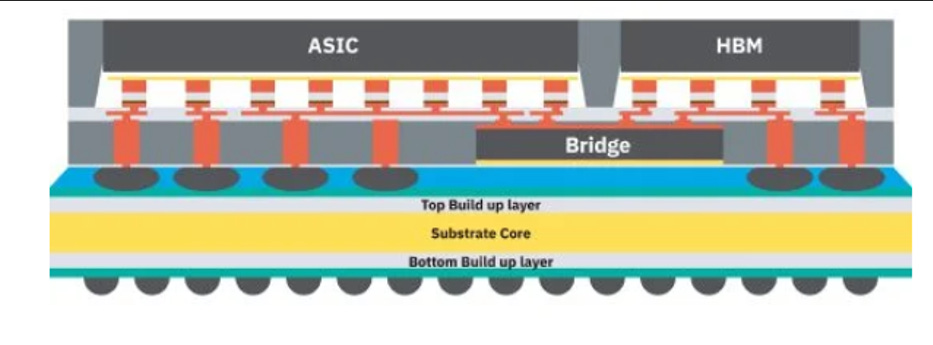

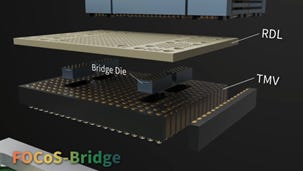

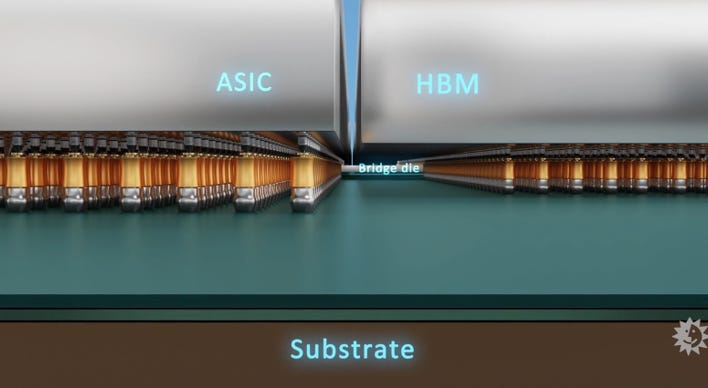

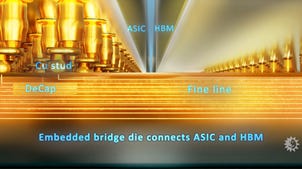

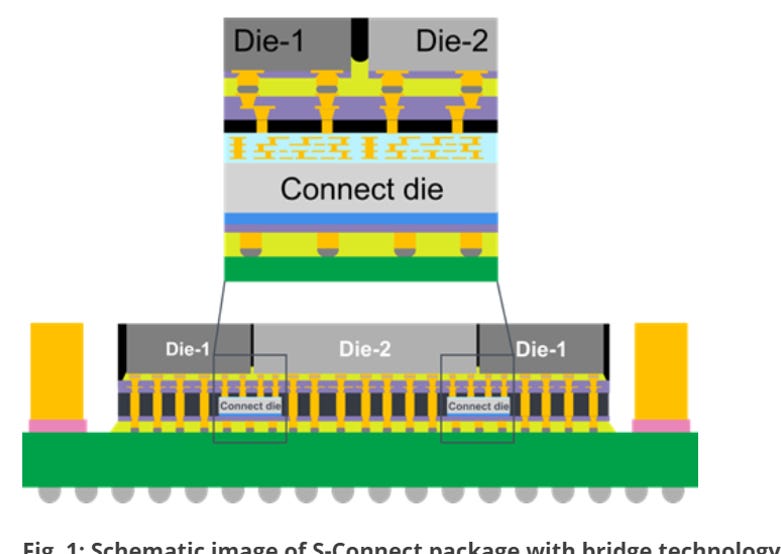

FOCoS bridge

Introduced 2023

Similar to FOCoS, but uses small silicon pieces with routing layers as ‘in package’ interconnects between chiplets e.g. between GPU and HBM

Provides similar electrical, signal, and power integrity performance to silicon interposer solutions

But at lower cost and without reticle size constraint

<1um L/S with die edge density of ~1000 wires per mm (of die edge) per layer

Compared to FOCoS of ~2um L/S with die edge density of ~500 wires/mm/layer

High I/O counts

However requires ArF or immersion DUV for silicon die bridge fabrication

Suitable for high speed signal transmission required for AI/HPC devices

Targeting AMD or ASIC AI accelerators

Silicon bridges provide ultra fine pitch interconnection in packages

Can address the memory bandwidth bottleneck challenges in systems

However, it only uses silicon pieces in the specific areas where the chiplets are being connected

Start with carrier wafer

Silicon bridge die is attached to carrier wafer using microbumps

Vertical copper posts then plated onto carrier wafer around the silicon bridge

Fabricated using semi additive process over patterned photoresist

Diameter 70um, pitch 150um, height, 80um

Epoxy mold compound (EMC) is then used to encapsulate the die and copper posts

Then grinded expose copper posts and microbumps of the bridge die

Dielectric then deposited

Through mold vias (TMV) etched down through the dielectric to reach the copper posts and bridge die microbumps

FOCoS bridge with TSV introduced in late 2025 which adds TSV in the bridge die to provide vertical delivery path

Reduce resistance by 72% and inductance by 50% v.s. standard FOCoS bridge

RDL layers are then formed

ASIC and HBM dies are then attached

Followed by underfill and molding

Carrier wafer is then removed

Then C4 bumps are attached on the now exposed bottom side

These connect to the original copper posts

Fan out wafer is then diced and singulated into individual packages

FOSiP (fan out system in package)

Next evolution beyond standard SiP

Dies are attached onto RDL instead of traditional substrate

Difference is that the interconnections are fanned out in RDL layer

As opposed to regular flip chip attachment for SiP

L/S typically 2/2um compared to regular SiP of ~10/10um

FOSiP can be thinner than regular SiP

Interconnections in RDL can have higher density, so requiring less layers than traditional substrate (about 3 layers reduction)

Also more cost effective as it utilizes wafer level packaging

Compared to placing components on individual substrates with standard SiP

Up to 60,000 units per hour

Use cases include wireless modules, IoT, Bluetooth/WiFi, and RF front-ends where high mix and high volume are required

Manufacturing process

Start with carrier wafer

RDL is fabricated first (i.e. chip last approach)

L/S of ≤2um

Built using semi additive process

Microbumps then deposited for chip to RDL interconnection

Also solder bumps added on backside of RDL for attachment to substrate

Chips and passive components attached onto RDL layer

Entire package is encapsulated using molded underfill (MUF)

Underfill and encapsulation are done simultaneously using mold compound

The mold compound fills the under-die gap during compression molding

As opposed to underfill being a separate epoxy step after die placement

Thin metal coating may be applied over mold cap for shielding sputtering

Provides EMI shielding for RF modules

2.5D/3D IC

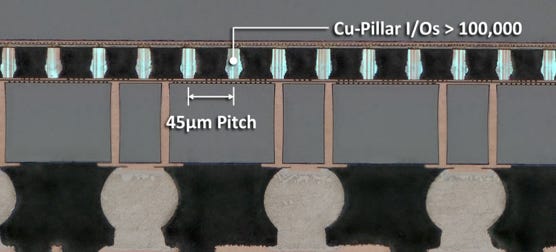

ASE also offers 2.5D packaging with silicon interposer on substrate

Similar to CoWoS-S

Silicon interposer is approx 100um thick

Ultra high density routing with L/S of 0.4/0.4um

Typically fabricated using 90nm/65nm

[Potentially outsource from UMC]

>100,000 copper pillar I/O with ~45um pitch

>400 microbumps/mm2

Interposer capable of embedding decoupling capacitor or active devices

Used for

High end GPU

High end FPGA

Network switch / router for data center & 5G infrastructure

AI accelerator for AI training/inference

Copackaged optics

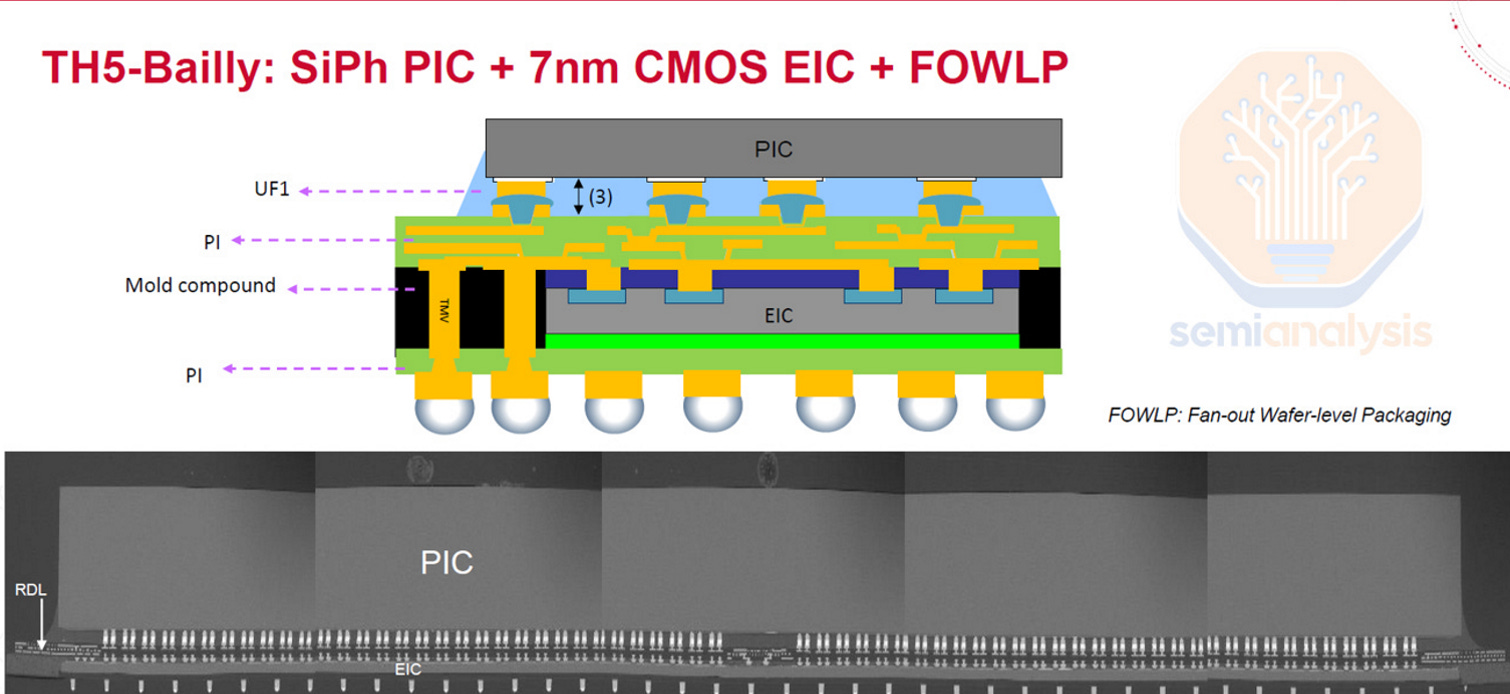

Broadcom reportedly transitioning from fan out wafer level packaging (FOWLP) with SPIL for is CPO solution to TSMC COUPE

FOWLP approach doesn’t allow scaling beyond 100G per lane due to excessive parasitic capacitance, as electrical signals must pass through the through mold vias (TMV) to get to the electric integrated circuit

Panel packaging

Have been working on panel packaging for over 6 years (2025)

Running pilot line for customer qualification for 600mm x 600mm late 2025/early 2026 (1Q25)

Testing

Largest provider of outsourced test services globally

Test services include

Wafer sort

Final test

System level test

Burn in

Currently primarily do wafer sort test. But have been investing to do final package test including burn in for late 2025/2026 (2Q25)

Can offer standalone test services, as well as combined full flow packaging and test service

Amkor

Known to be leader for automotive OSAT

Decades of experience meeting the stringent requirements of auto industry

E.g. Automotive certification (AEC-Q100) requires robust assembly

Have key facilities in EU and Japan

Manufacturing

Have fungibility of equipment between 2.5D advanced packaging types including

With silicon interposer

With RDL interposer

With silicon bridge embedded in interposer

Vietnam

Started production in 3Q24, ramping in 4Q24

Chosen for low cost structure

Mainly for consumer device market i.e. SiP

But also NAND and some 2.5D coming online (2Q25)

Migrated some SiP from Korea to Vietnam

To free capacity in Korea for advanced packaging

Act as second source alternative to China

5 of top 10 customers are qualifying Vietnam

Started with 2 lead customers

South Korea

Setting up to be able to do packaging and testing at the same place

Broke ground on new building in late 2025

Investing in tester fleet for high density digital pins and power supplies (2Q25)

Include burn in, SLT, and temperature stability handling systems

Phase 1 projected to be operational by end of 2025

Add 4000-6000 sq ft of test floor

Phase 2 est 1H27

Est to add another 40% capacity

Equipment moving in end of 2026

Bringing online 2.5D technology (2Q24)

Also have R&D facility

Japan

Mainly for auto and industrial packaging lines

Began to rationalize packaging lines (3Q25)

Due to underutilization in the auto market

Mainly in the mature side i.e. microcontrollers and traditional analog products

Note, did a similar rationalization in 2022

Closed 3 locations and reduced headcount

Working closely with customers on the taper down

Will raise prices for customers that remain to manage profitability

Will expect to finish taper down by 2027

Expect 100 bps improvement in company gross margin %

Portugal

In support of EU auto sector

Include advanced power modules such as SiC, GaN

Have partnership with Infineon

Arizona, US

Total $7b investment earmarked

Increased from $2b announced initially

Total 750k sq ft of clean room space

Most of capex will come in 2026 and 2027

Will be built in 2 phases

Phase 1

Broke ground in 3Q25

Est $2b investment

Expect to be completed mid 2027, with ramp in 2028

Est to be accretive to profitability 2 years after (i.e. 2030)

Est to contribute 10% of revenue

Phase 2

Announced phase 2 due to additional demand for US onshoring

Timing will be dependent on demand

Will be constructed with automation in mind

Will be located close to TSMC fab location

Will align TSMC technology nodes with Amkor packaging technology

However, not exclusive to TSMC

Amkor can also go direct to customers

CHIPS Act grant and investment tax credit would total approx $800m

Grant money will have a lag until it is received

Cost to be managed using

Level loading agreements

Guarantee stable, and consistent wafer volumes over time (e.g. X wafers/month or quarter)

Will help maintain high utilization

Low mix, high volume focus

Turnkey services

High automation

Also investing in testing facilities

Go to market

Have joined TSMC 3D Fabric Alliance (2022)

Signed agreement with TSMC to collaborate with TSMC on advanced packaging and testing in Arizona, US (2024)

Jointly define which packaging technologies to employ

Will effectively share end customers

Include some level of technology sharing

Likely to include Apple and Nvidia

Designed Process Assembly Design Kits (PADKs) and a design flow to achieve electronic design automation (EDA) connectivity with Cadence and Mentor Graphics

This is because designing chips need to have manufacturability and packaging in mind (i.e. design for manufacturability)

Packaging

Offer over 3000 different package formats and sizes

TSMC outsourcing

It is believed that Amkor also does a share of the wafer on substrate (WoS) portion of CoWoS

Split share with ASE Technology

Amkor will likely take 100% share of any TSMC CoWoS outsourcing at the Arizona, US fab

Completion scheduled for mid 2027

May also be outsourced the full flow for CoWoS

SiP (system in package)

Offers multi component, multi function products in an IC package

Embedded passive and active components

Offer double sided assembly

Chips attached on both sides of substrate

Include antenna in package (AiP) solutions

Amkor serves both iOS and Android market

Has been working with Apple for >10 years as SiP provider (for communications or RF)

Rumored to have lost mmWave AiP module for iPhone 15/16 generation (2024)

But then regained it back in 3Q25

SLIM (siliconless interconnect module)

2.5D

Amkor provides 2.5D packaging with silicon interposer with TSV

However note that Amkor does not manufacture the TSV themselves

Instead, they take wafers that have TSV already formed from foundry

“It is essential to distinguish that Amkor does NOT provide TSV formation in foundry wafers” ( https://amkor.com/technology/25d-3d-tsv/)

Amkor takes wafers in which ‘blind’ TSV have already been formed

It is ‘blind’ in the sense that the TSV stops partway through the silicon

I.e. you cannot see the TSV from the backside (until you thin the wafer)

Then thin wafer to expose TSV to complete the TSV interconnect structure

Wafer may start around 775um thick, then thinned down to 50-100um depending on the design

Then complete backside metallization to complete the connection to TSV

It is implied from earnings calls that Amkor provided packaging for Nvidia H20

Amkor notes that it has expanded customers from 2 to 4 (Nasdaq conference, Dec 25)

Increased revenue 4x from 2023 to 2024

Currently around single digit % of revenue (2Q24)

[Rumored to include Broadcom for networking and TPU in 2026/27]

[Also Nvidia GB10 for DGX Spark]

WLFO (wafer level fan out)

Licensed eWLB (embedded wafer level ball grid array) technology from Infineon

Similar to TSMC InFo and ASE FOCoS

Die is placed onto carrier, embedded in mold, and then RDL formed directly on top

Solder balls then attached to RDL, which is attached to substrate

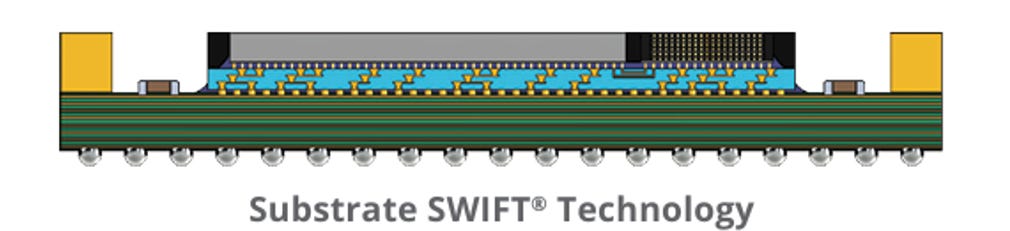

SWIFT (silicon wafer integrated fan out)

Amkor’s technology for high density fan out wafer level packaging

L/S of 2/2um

S-SWIFT (substrate-SWIFT or silicon wafer integrated fan out on substrate)

Equivalent to TSMC InFO-R

Flip chip chips onto RDL, then mounted on to BGA substrate

Supports >1,000 I/Os

2-6 RDL layers

Provide lower cost alternative to TSV 2.5D

Used for high I/O devices such as networking and server chips

Engaged between 5-10 customers (2Q24)

Launched with 1 existing customer and 3 new customers (1Q24)

First customer ramped (3Q25)

Second customer qualified and beginning ramp (Dec 25)

S Connect

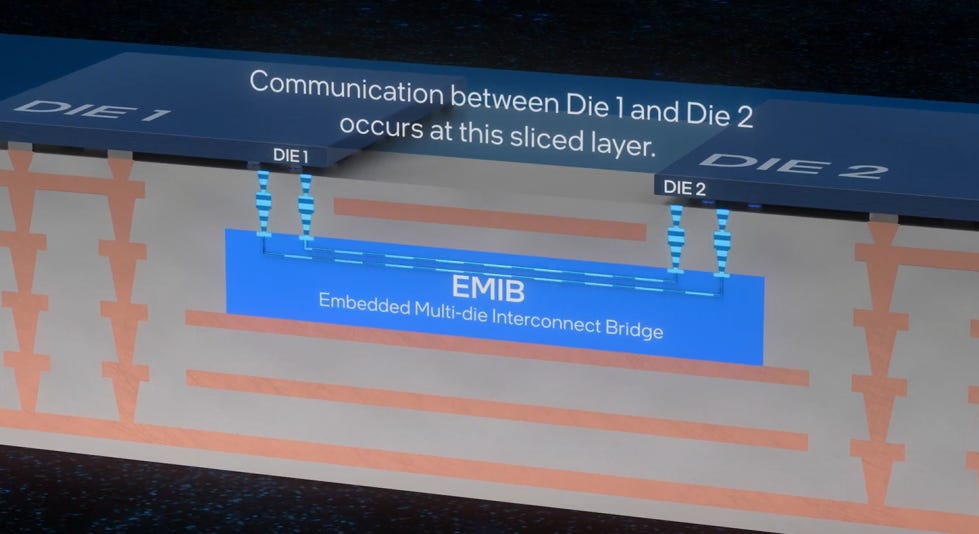

Uses embedded silicon bridge embedded in fan out structure

Similar to Intel EMIB and TSMC CoWoS-L

Silicon bridge can either be connected using microbumps or TSV

TSV used for ASIC + HBM integration

Supports integrated passive devices (IPD) embedded in mold

Power delivery line from top die to substrate can be connected using through mold vias (TMV)

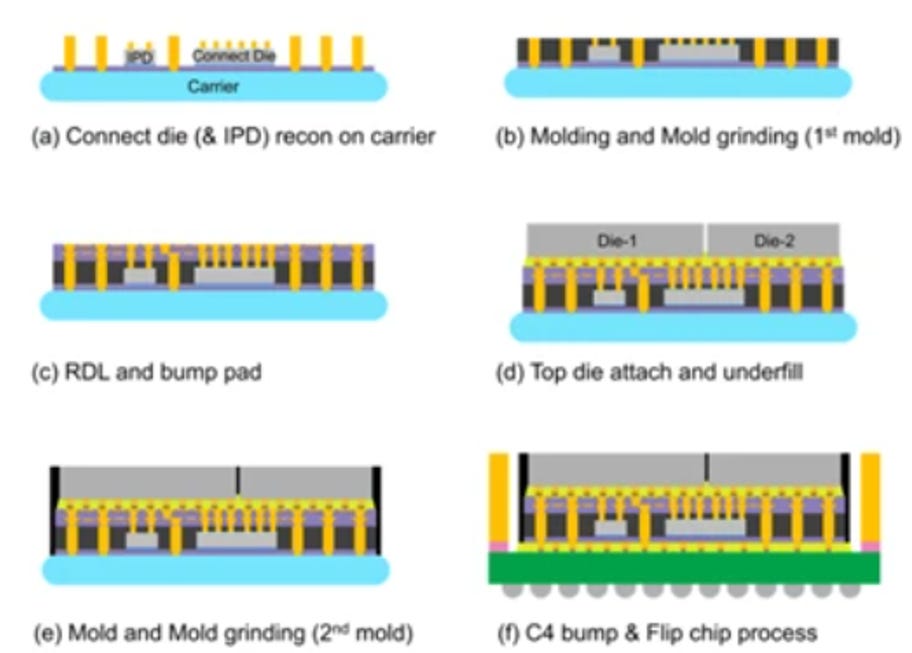

Utilizes RDL first/chip last process

Silicon bridge die, IPD and copper pillars connected onto carrier wafer

Then encapsulated with mold and grinded to expose copper connections

RDL then fabricated on the mold

Top die attached to RDL with microbumps

Package then encapsulated again with mold

Carrier wafer then removed

C4 bump then added and attached to package substrate

Have 2 customers in qualification

Expected to ramp 2026 (1Q25)

Testing

>3600 testers in 8 locations

Additionally, have >600 cosigned

>10b units and >1.8m wafers tested annually

Operate 24/7 on fully networked test floors (i.e. software connected environment)

ATE, handlers, probers, data management tools are coordinated and centralized

Dynamic scheduling of test jobs across available ATEs

Test cell pooling across product families

I.e. multiple product types share the same pool of test equipment

Remote monitoring and control

Typically co located with packaging

Provides efficiency and avoid moving between countries

Can provide geographical diversification as most of global test capabilities is in Taiwan

Typically generate margins above corporate average

Known for RF test services

TSMC

TSMC has significantly gained share in advanced packaging, primarily due to integration of front end and back end processes for Apple and Nvidia

Apple is the key customer for InFO and Nvidia is the key customer for CoWoS

InFO (integrated fan out)

InFO-R (RDL interconnect)

Used for Mac M series chips (e.g. M1, M2, M3)

Typically 2-5 RDL layers

InFO-SoIS (system on integrated substrate)

Up to 14 RDL layers

However avoids using conventional ABF substrate stack up

Enable complex wiring between layers

InFO-SoW (system on wafer)

Allow fan out to the size of the entire wafer

E.g. Tesla Dojo 1

InFO-L (local silicon interconnect + RDL)

Include silicon bridge beneath the dies

Can be either passive (metal routing) or active (contain transistors)

First used in M1 Ultra to connect multiple M1 Max chips

Apple branded it ‘UltraFusion’ architecture

>10,000 signals between dies with 2.5TB/s of die to die bandwidth

Later also M2 Ultra

InFO PoP (package on package)

Can stack memory on top of processor

Used to reduce thickness and improve thermal efficiency

Used for Apple iPhones starting with A10 (iPhone 7)

Also Apple Watch S series

SPIL reportedly lost Apple’s A10 packaging to InFO in 2016

InFO oS (on substrate)

Designed for integrating multiple logic chiplets onto a substrate

Used for networking SoC, and HPC accelerators that want to avoid costly silicon interposer

InFO AiP (antenna in package)

Integrates the antenna directly into the chip package

Reducing size and improving signal gain and electrical performance

Used in 5G mmWave front end modules

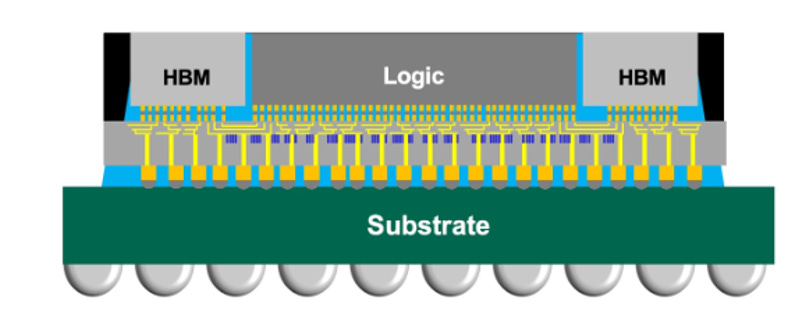

InFO MS (memory on substrate)

Designed to integrate HBM with HPC logic dies

Wafer level multi chip module (WMCM)

Evolution from InFO

Unclear what the exact structure is

To be adopted for A20 chip used for iPhone 18 on 2nm process

Expected 3Q/4Q 2026

Will also use molding underfill (i.e. integrates the underfill and molding processes)

CoWoS (chip on wafer on substrate)

CoWoS-S (silicon interposer)

Interposer area has increased up to 3x reticle limit

Use of reticle stitching

Uses embedded deep trench capacitor (eDTC) integrated into the silicon interposer as a passive device

Deep trench structures etched into the silicon interposer

Filled with high density dielectric to form capacitors

Used to smooth voltage and maintain signal integrity

As chips operate at very high currents and high frequencies

Help deliver stable power and reduce voltage droop

New thermal interface material (TIM) for lid package

Server ODMs were overtightening the cooler screws

Caused the die to crack

So TSMC used a package that had a lid ‘over’ the die rather than directly on the die

Used for Nvidia Ampere A100 and Hopper H100

CoWoS-R (RDL interposer)

Silicon interposer replaced with organic RDL